These ambitions are exemplified by MC’s $5.2bn (¥821bn) acquisition of Aethon—one of the largest privately-held gas producers in the US—in January this year. The company’s largest deal to date, this marks a strategic step in further strengthening its integrated energy and power value chain.

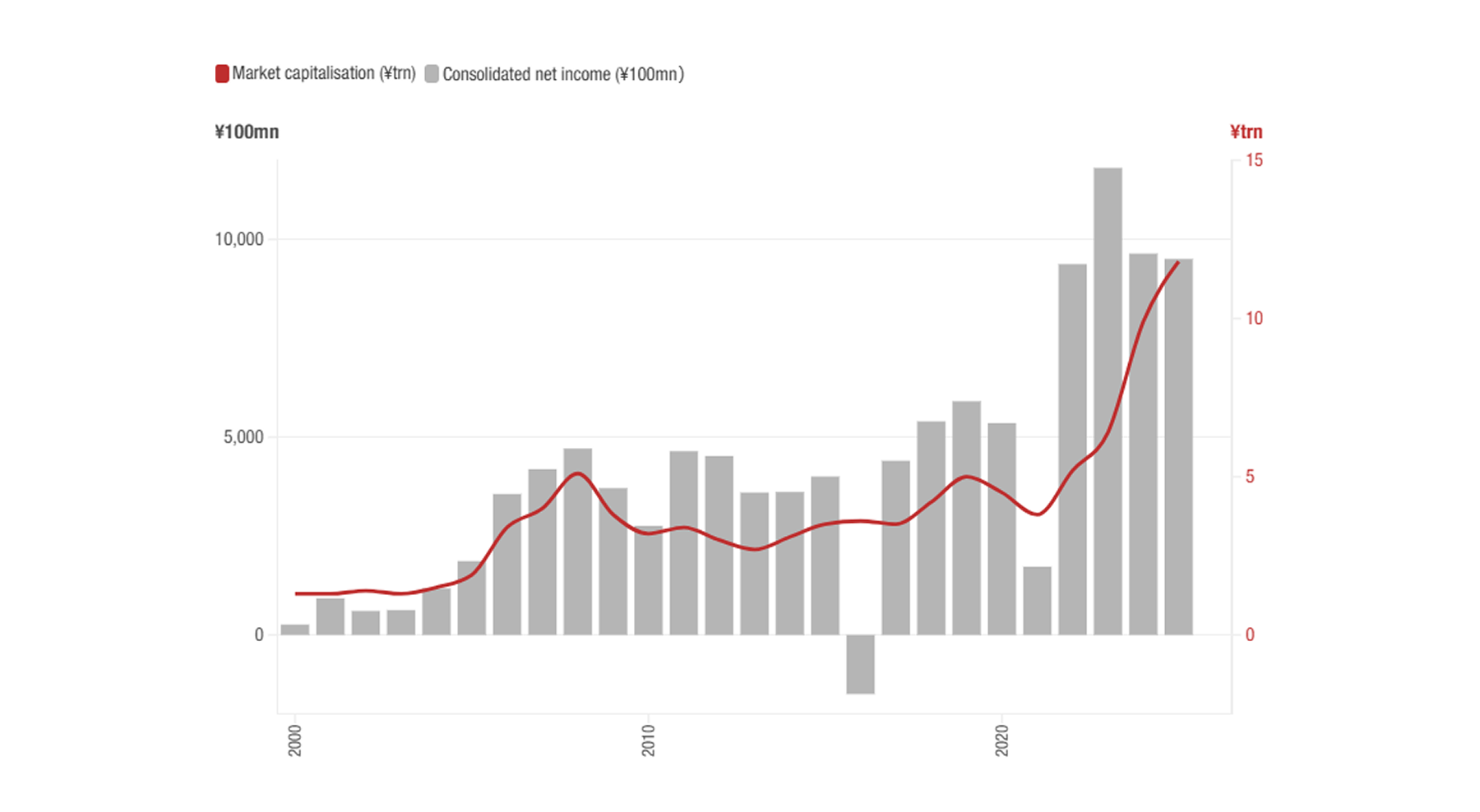

MC’s disciplined strategy has supported steady earnings growth, a moderate debt-to-equity ratio and attractive payout ratios, while boosting its market capitalisation more than tenfold over the past 25 years, achieving a net income of $6.03bn (¥950.7bn) in FY2024 and a market capitalisation reaching the $127bn (¥20trn) level in early 2026. This performance underscores the company’s ability to leverage its strengths as a sogo shosha—Japan’s general trading and investment model.

The growth of Mitsubishi Corporation's market capitalisation

The evolution of the sogo shosha

The sogo shosha are unique to Japan, emerging in the aftermath of World War Two. Under the new global trade environment, resource-scarce Japan had little choice but to expand its import and export activities. MC became central to this effort: in its early years, the company played a vital role in securing much-needed stable supplies of energy and raw materials to support the country’s manufacturing sector, while also handling export trade in machinery, chemicals, and processed foods—areas where Japanese technology held a strong competitive edge—thereby contributing to the development of industries across the economy.

As the economic landscape evolved, so did the sogo shosha. To adapt to macroeconomic shifts and declining profitability in traditional trading, MC reinvented its business model, pivoting towards active business management and strategic investments in sectors ranging from mining and liquefied natural gas (LNG) to retail such as convenience stores.

Today, MC continues to advance this transformation by focusing on resilient, future-oriented business models. Between FY2022 and FY2024, the company invested $18.4bn (¥2.9trn), with part of this allocation directed toward critical minerals and digital infrastructure.

These strategic moves signal a growing commitment to advanced technology and more resilient investments, an approach further reinforced by the Aethon deal.

Value in integrated strength

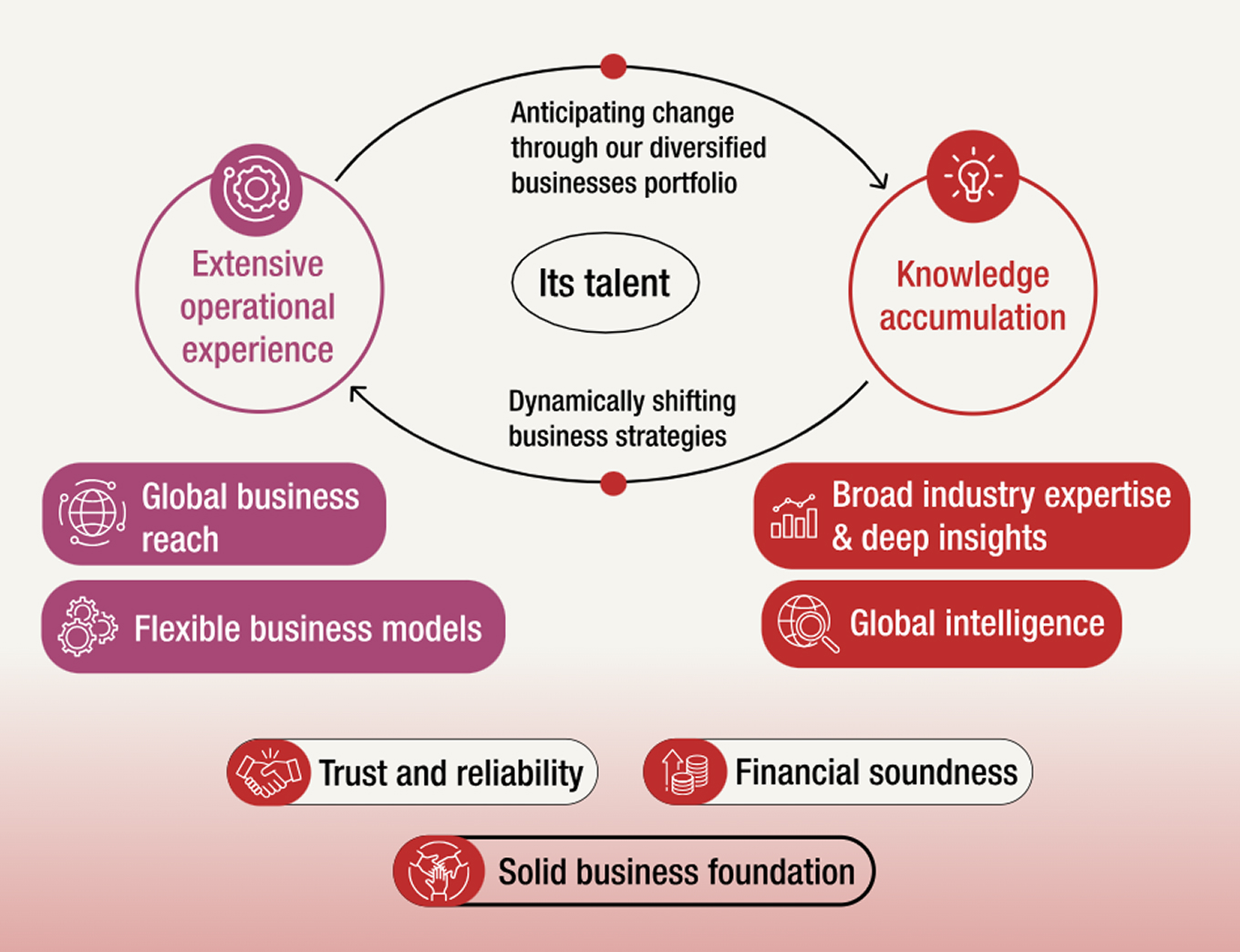

In 2025, MC ushered in a new era with the unveiling of its Corporate Strategy 2027, under the theme “Leveraging Our Integrated Strength for the Future”. At the heart of this strategy is the company’s concept of “integrated strength”: the notion that MC’s competitive advantage lies in the sum of its parts, in addition to individual businesses across its portfolio. This approach enables the company to dynamically shift business strategies in anticipation of change.

"Beyond strengthening their individual business activities, our business segments aim to collaborate and combine their capabilities to generate synergies,” says Katsuya Nakanishi, Chief Executive Officer at MC. “As the business environment continues to evolve and new opportunities emerge, we are focused on pursuing new cross-industry integrations.”

MC's Integrated Strength

According to Mr Nakanishi, this fusion of strengths has enabled MC to stay ahead of the curve. As the company navigates an increasingly uncertain business landscape, its “integrated strength” will help it create new revenue streams that enhance corporate value.

continues to evolve and

new opportunities emerge,

we are focused on pursuing

new cross-industry integrations.” Katsuya Nakanishi,

Chief Executive Officer, Mitsubishi Corporation

Investing for value creation and growth

As outlined in Corporate Strategy 2027, MC assessed how rising global volatility is reshaping the markets in which its businesses operate, and concluded that maintaining sustainable growth hinges on balancing adaptability with organisational stability and strategic clarity. The strategy therefore provides a long-term vision while allowing room for flexibility as the business landscape continues to shift.

The strategy is anchored in three key initiatives that will guide how the allocation of the company’s planned $25.4bn (¥4trn) of investments between FY2025 and FY2027.* The first initiative, “Enhance”, focuses on reinforcing the profitability of existing businesses through expanded operations and investments. A recent example is MC’s acquisition—through its wholly owned subsidiary Cermaq—of three salmon farming operations from Grieg Seafood in Norway and Canada, a move that will boost Cermaq’s production capacity to roughly 280,000 tonnes by FY2027, elevating it to the world’s second-largest salmon producer.

The second initiative, "Reshape”, includes investments and capital strategies aimed at preparing portfolio businesses for potential market shifts. In one case, Anglo American Sur (AAS), in which MC holds a 20.4% stake, has entered into a definitive agreement with Codelco to implement a joint mine plan to maximise operational synergies while increasing annual production, a move that anticipates burgeoning global demand for critical minerals.

Finally, under the “Create” pillar, MC plans to identify new investment opportunities that will synergise its existing business domains, such as in LNG and the bio-resource value chain. Notably, the acquisition of Aethon is projected to boost the company’s earnings, marking significant progress toward the strategy’s quantitative targets. From this investment, underlying operating cash flow is expected to reach approximately $1.7bn to $1.9bn (¥270bn to ¥300bn) in FY2027, while consolidated net income is projected at around $444m to $508m (¥70bn to ¥80bn).

With electricity demand set to surge with the artificial intelligence (AI) boom, natural gas will play a critical role, ensuring secure, cost-competitive energy and serving as a bridge in the transition to decarbonisation. Against this backdrop, MC is well-positioned to enhance Aethon’s profitability, drawing on its extensive experience across the energy value chain, particularly in the North American market.

The acquisition of Aethon also opens pathways for cross-sector synergies beyond energy, including opportunities in power generation, gas chemicals and data centres. This forms part of MC’s broader efforts to build an integrated natural gas value chain capable of addressing global energy challenges.

The next chapter

MC’s endeavour to evolve has delivered clear results, and the trend is set to continue. In line with its corporate strategy, it is on track to achieve an average operating cash-flow growth rate of 10%, and an ROE of 12% or higher. The company’s ability to connect diverse businesses, orchestrate complex value chains, and unlock long-term growth opportunities remains central to its continued success.

But the current era of uncertainty is marked by transformative shifts that transcend traditional industry boundaries. For example, in the automotive sector, an industry which MC has significant investments in across Southeast Asia, the advancement of autonomous driving is fundamentally reshaping industry structure, shifting key differentiators from hardware to AI and software. Such shifts are playing out across sectors, and as traditional industry boundaries are becoming less defined, MC is leveraging its strengths by being adaptable and developing businesses across sectors.

By engaging across a wide range of touchpoints in multiple industries, MC’s strengths across the value chain reinforce its ability to create cross-sector opportunities, giving the company a clear competitive advantage. The acquisition of high-potential businesses such as Aethon illustrates how MC’s multifaceted “integrated strength” enables it to generate value that extends beyond a single sector or entity. Unlocking the breadth of this potential, while turning change into opportunity and opportunity into action, positions MC for continued growth and long-term value creation.

Produced by EI Studios, the custom division of Economist Impact